Insurance Companies Bear the Blame

Voters tie health care affordability pressures mainly to rising premiums and out-of-pocket costs – and say insurers bear the most responsibility.

Key Takeaways

Voters define the health care affordability crisis primarily through insurance costs.

Premiums are the dominant concern, followed by out-of-pocket costs.

Insurance companies are seen as the primary source of financial strain and most in need of fixing, though providers do not escape blame.

Overall, insurers are viewed as most responsible for voters’ top concerns.

The cost of health insurance premiums is by far the biggest concern of voters when it comes to health care, both when specifically asked about health care costs and the state of health care in the United States overall. Out-of-pocket costs, waste, fraud, and abuse, prescription drug costs, and surprise bills rank as second-tier concerns.

Most voters say insurers are more responsible for premiums and out-of-pocket costs, while voters more often blame the entire system for surprise bills and waste, fraud and abuse.

Why it Matters

Recent America’s New Majority Project surveys ranked health care costs as voters No. 2 economic concern and showed the popularity of reforms increasing transparency and patient control of their health care dollars.

These results reinforce earlier results: premiums should be the central affordability focus, and insurers the primary reform target.

For candidates, appearing to let insurers off the hook is a clear liability.

How to Use This Data

Messaging should lead with lowering monthly premiums and holding insurance companies and middlemen accountable. Health care agendas should clearly answer the question: “How does this lower premiums, reduce out-of-pocket costs, and increase health insurer accountability?”

Click on the image below to view the full data or read the summary below.

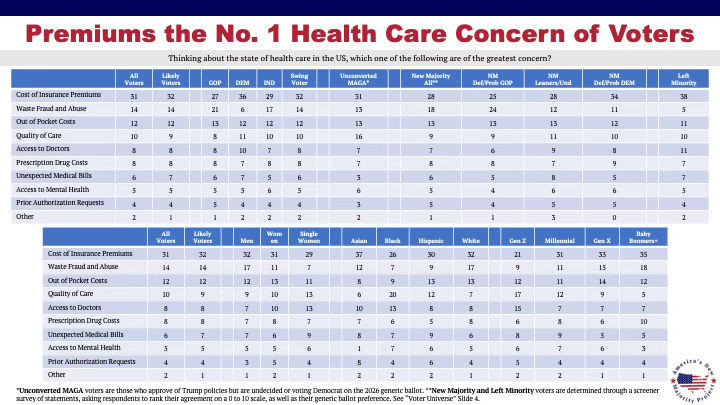

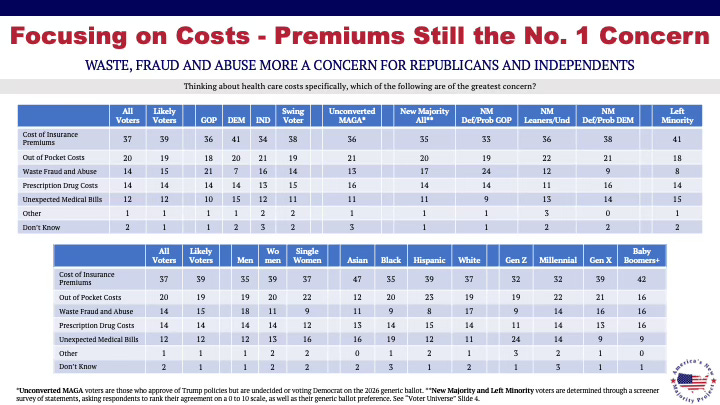

Premiums Are the No. 1 Health Care Concern

31% say the cost of insurance premiums is their greatest concern when it comes to the state of health care in the United States. Focusing on health care costs alone, 37% say premiums are the top concern.

The cost of premiums is the top health care cost concern of all demographic groups, with Democrats (41%) and Baby Boomer and older voters (42%) most concerned.

Out-of-pocket expenses (20%), waste, fraud and abuse (14%), and prescription drug costs (14%) are second-tier concerns. Notably, Republicans and independents are significantly more focused on waste, fraud, and abuse than Democrats.

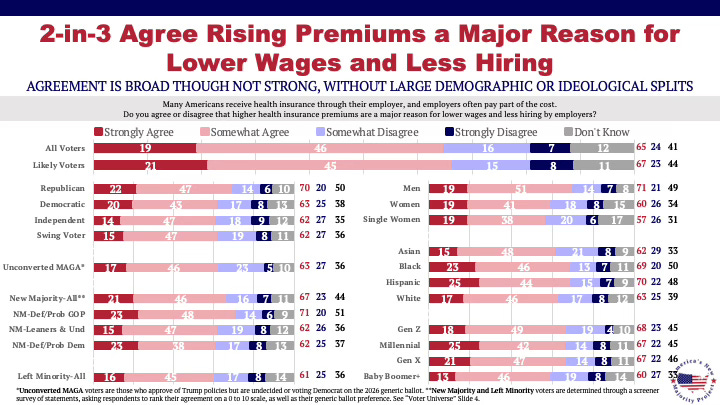

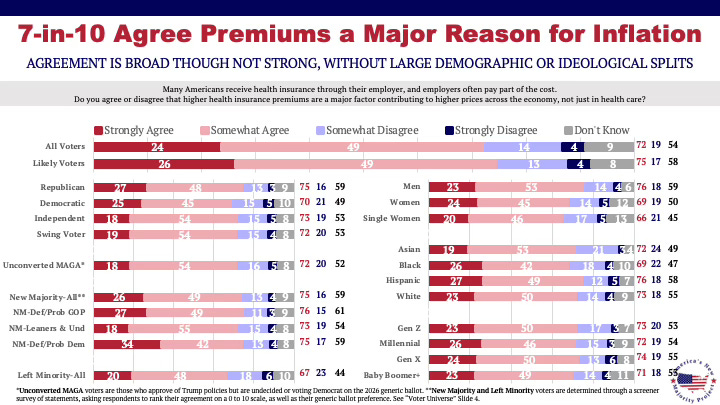

Rising Premiums Seen as Economy-Wide Burden

65% of voters agree that higher health insurance premiums are a major reason for lower wages and less hiring, with strong agreement at 19%.

This agreement is shared by a majority among all demographic groups, with minor ideological and partisan differences in intensity of belief.

72% agree that higher health insurance premiums are a major factor contributing to higher prices throughout the economy, not just in health care, with strong agreement at 24%.

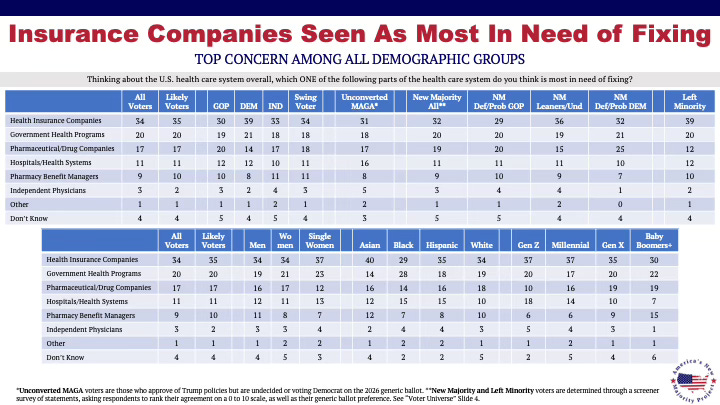

Health Insurers Seen as Most in Need of Fixing

34% say insurance companies are the part of the health care system most in need of fixing.

It was the top choice of all demographic groups with Democrats (39%) and younger voters (Gen Z: 37%, Millennials: 37%) the most focused on insurance companies.

Government health care programs (20%) and drug companies (17%) are second-tier targets for reform, with older voters (Gen X: 19%, Boomers: 19%) more focused on drug companies than younger.

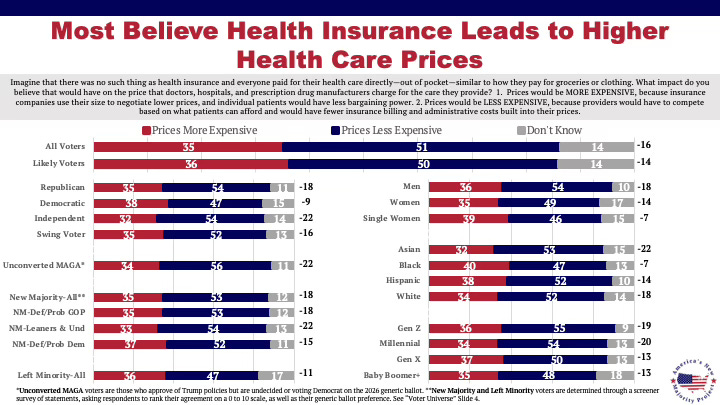

Health Insurers Seen as Cost-Adders, Not Cost Savers

Respondents were asked to imagine the impact on health care prices if health insurance didn’t exist and everyone paid for health care directly out-of-pocket.

51% said prices would be less expensive, while 35% said prices would be more expensive.

Demographic differences in responses were small, suggesting that how respondents answered had more to do with their personal experiences than ideological or partisan worldview.

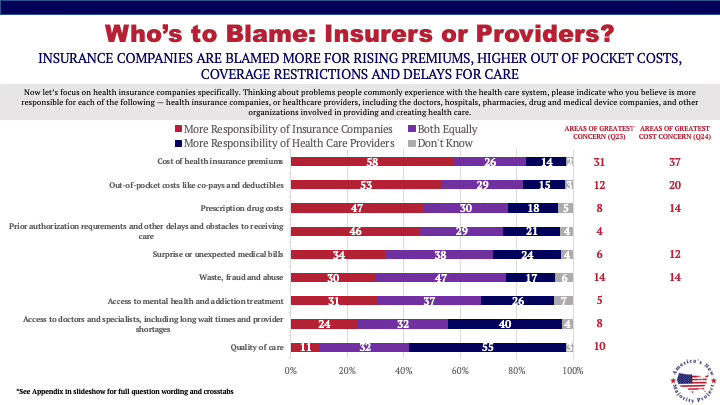

Who Voters Hold Responsible

Returning to the areas of most concern in the health care system, respondents were asked who was more responsible: the health insurance companies or the health care providers (including the doctors, hospitals, pharmacies, drug and medical device companies, and other organizations involved in providing and creating health care.)

58% of voters say health insurance companies are more responsible for the cost of premiums, including a majority or plurality among all demographic groups.

53% say health insurance companies are more responsible for out-of-pocket costs, including a majority or plurality among all demographic groups.

A plurality of voters also say health insurance companies are more responsible for prescription drug costs, coverage restrictions and delays to getting care.

Health care providers were seen as more responsible for quality and access challenges, not financial burdens.

Target voters – Unconverted MAGA and New Majority Undecideds and Leaners – were more inclined to blame both insurers and providers than other demographic groups for the cost of premiums and out-of-pocket costs, though more still blamed insurers.

The Bottom Line

Premiums are the central affordability concern, and voters across every demographic agree.

Insurance companies bear the blame: majorities say insurers are more responsible than providers for both premiums and out-of-pocket costs.

Notably, a majority believe health care would be cheaper without insurers in the mix. Voters support reform that directly confronts both the cost and the cause.

What’s Next

We will have more analysis from this survey identifying the health care reforms Americans say should be lawmakers’ top priorities, new data on apprenticeships, and more.

We want to hear from you! We not only enjoy hearing from our subscribers, but we also use your feedback to bring you the most recent and engaging policy information available. Share how you’re using this data or tell us what new insights you’d like to see.

Get in touch with us anytime, and let’s make an impact together!

This is a pet peeve of mine. Of course insurers are the source and origin of the chaos that now defines our medical delivery system. They are the hat trick; the ones who make money from other people's misfortune without incurring any real risk other than financial exposure. They buy and sell fear. The opportunities for abuse within the insurance industry are legion, and built in.

Consider the scenario:

You have a good job making a living wage. You are married with children. You have a mortgage, (which is another industry fraught with opportunities for abuse), and children. Your kid breaks a leg. You take your kid to your family General Practitioner, who has an office in the basement of his home 3 blocks away. He handles these kinds of accidents routinely with expertise. He charges a set fee that he has calculated based on his costs and a fair price for availability and expertise. You take your kid home, he recovers, you go back to get the cast removed, your kid is fine and he goes back to his life a bit wiser.

Now add insurance abuse. First, how did he break his leg? Sue them. Oh, it was his school? He fell off the jungle gym? Did they have insurance? It was off-hours? They need more. They counter sue. Lawyers get involved. Does everybody have insurance to pay the lawyers? And what about that doctor? What if something goes wrong? Does he have malpractice insurance? Is his office adequately covered? What if the kid's leg gets infected while he's there? Check his education and his licenses. Maybe the kid broke his leg while playing football during gym class? Can we sue the school? On and on and on. The trick is to generate fear, and then buy it from your "customers".

All of these scenarios are valid and have played out many times in the courts. The problem is with intangibles; ethics, morality, honesty, justice, transparency, goodness, and elusive concepts like "value", "compassion", and "circumstances".

While we argue over which service is to "blame", we fail to address the forces that color our perception of the circumstances that affect our response. Let's add some color.

The marriage is not great. There was an argument. The kid ran out to get away. He went to the school because he feels safe there. It's after school hours when he falls off the jungle gym. A neighbor finds him and carries him to a doctor she knows nearby. The doctor knows that it would be hours if they go to the Emergency Room, and he has an office in the basement for minor cases like this. When they get in touch with the parents, they find that alcohol is involved, and the parents see an opportunity to cash in on the doctors insurance.

You see where I'm going? The facts have colored our perception.

Life is not simple. A large part of what's missing from our current system is intangible. We need to quit searching for a perfect solution, and begin to embrace the difficult things, like love, forgiveness, compassion, insight, and understanding.

The medical professions are much closer to these aspects of life. The insurance industry is ALMOST irreparable, due to its abstract nature. It needs a serious take-down.

548560