Voters Prioritize Insurance Company Accountability in Health Care Reform

Voters want reforms that curb insurer steering, increase transparency, and guarantee savings reach patients.

Key Takeaways

Voters prioritize insurance-focused reforms: curb steering, increase transparency, ensure savings reach patients.

Insurer and middleman accountability is the strongest performing center-right message.

Most voters believe insurer-provider integration raises prices and a plurality supports limits on insurer ownership.

Voters oppose penalizing patients for choosing lower-priced, independent providers.

Voters prioritize reforms targeting insurance companies — especially proposals that curb insurer steering, guarantee savings flow directly to patients, and increase upfront transparency on total and out-of-pocket costs. Reflecting these priorities, among four center-right positioning statements tested, the message emphasizing insurance company and middleman accountability performed best.

Most voters also believe vertical integration in health care — particularly insurer ownership of providers — raises patient costs.

Why it Matters

Recent ANMP surveys show health care costs are voters’ No. 2 economic concern, driven largely by rising premiums and out-of-pocket costs. Voters consistently blame insurance companies more than other parts of the health care system for affordability challenges.

These findings identify which reforms prioritize most and which candidate messages generate the strongest support.

How to Use This Data

Candidates and advocates should frame health care reform around:

✓ Increasing insurer and middleman accountability

✓ Protecting patients from unfair practices

✓ Guaranteeing savings reach patients

View the full data by clicking below, or read key highlights in the summary.

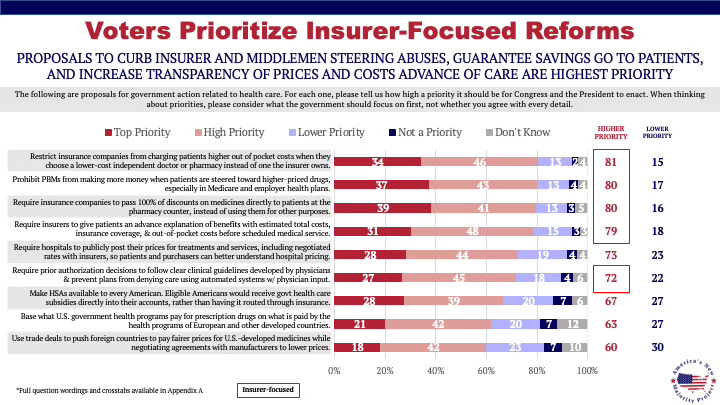

Voters Prioritize Insurer-Focused Reforms

Reforms targeting insurer steering, passing savings directly to patients, and enhancing transparency draw the broadest support from voters.

The most intense support, with 39% saying it is a “top priority,” is for requiring insurance companies to pass 100% of discounts on medicines directly to patients at the pharmacy counter.

Prohibiting PMBs from making more money when patients are steered toward higher priced drugs is the next most intense – with 37% saying the reform is a top priority.

Demographic differences by party and race are minimal. Older voters react more intensely to reforms they see as saving them money on prescription drugs.

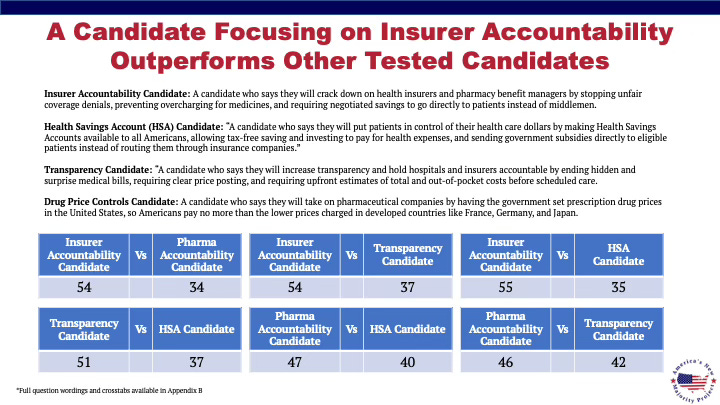

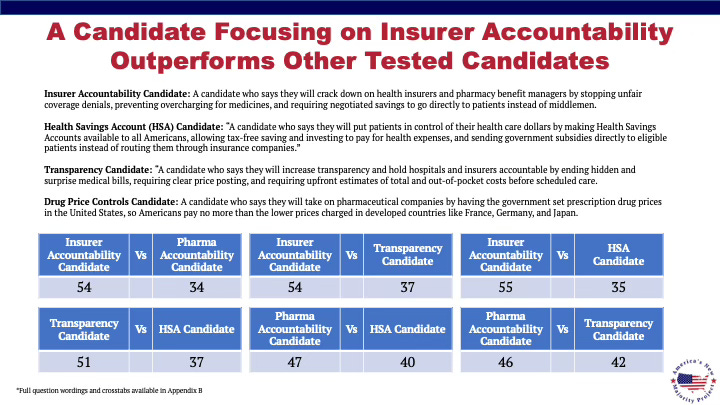

Insurer Accountability Message Tests Strongest

A candidate focused on curbing insurer and middleman abuses and requiring savings to be passed directly to patients tests strongest out of the four positioning statements tested, defeating the other three candidates by a roughly 20-point margin.

Candidates focused on price transparency and drug price controls were less effective, while a candidate focused on expanding Health Savings Accounts (HSAs) tested the worst.

These results strongly reflect the priority level voters give to certain reforms, not their overall popularity.

Independents favor the transparency-focused candidate more than other demographic groups, though the insurer focused candidate still performs best with them.

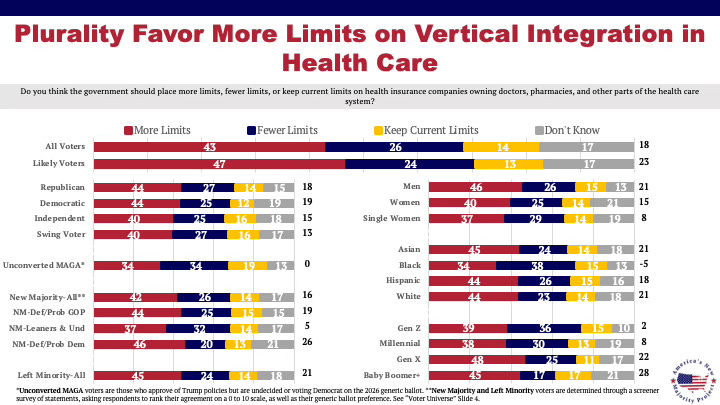

Voters Skeptical of Vertical Integration in Health Care

59% believe vertical integration in health care – specifically insurers owning providers and other parts of the system – makes health care more expensive.

68% say insurers should not be allowed to charge patients higher out-of-pocket costs if they choose a lower priced, independent provider not owned by the insurer.

43% – a plurality – favor more limits on insurers owning other parts of the health care system. 26% oppose.

Demographic differences by party are minimal, but there are some differences by race and age. Black voters make up the only group who believes fewer limits should be placed on this sort of ownership, while older voters are more likely to favor more limits than younger.

The Bottom Line

Health care reform messages centered on insurance company accountability, patient savings, and transparency generate the broadest and most intense voter support. Candidates emphasizing insurer and middleman crackdowns hold a clear advantage over those focused primarily on transparency, drug pricing, or HSAs.

What’s Next

We will have more analysis from this health care survey, data on apprenticeships, and more.

We want to hear from you! We not only enjoy hearing from our subscribers, but we also use your feedback to bring you the most recent and engaging policy information available. Share how you’re using this data or tell us what new insights you’d like to see.

Get in touch with us anytime, and let’s make an impact together!

The insurance companies aren't the only problem. Private equity investment and large provider organizations that hoover up small independent practices contribute to price increases and lack of competition. The market is utterly distorted by government regulation, insurance companies, and outfits like the Cleveland Clinic. There's little hope for relief in the USA simply because of the massive amount of monied interests involved in the "industry".

Where we have experienced health care that works is in places where health care is viewed as a public service and not as a profit center for insurance companies or private equity peeps. South Korea has an amazing system. Until recently all hospitals were required to be operated as non-profits. This is NOT social medicine. While health care providers are all private, the government runs the funding scheme. Everyone is required to pay into the system (about $100 per month) and at time of treatment there are small co-pays or additional fees. A two view X-ray at a major hospital cost us $21. Cleveland Clinic quoted us $950 for the _same thing_. Hospitals have to compete for patients since they are paid on a per patient service basis and not a flat rate over time. So hospitals in Korea have become very efficient at serving patients. A wait to see a provider in a hospital of more than 3 or 4 days is unusual. Small clinics see patients on a walk-in basis, same day service. Try THAT in the USA.

Here in Taiwan the system is similar to Korea's. Our monthly payment is about $58. Oh, and this covers vision and dental as well. Prescriptions are reasonable. One that costs us $75 in the USA only costs $8 here. The co-pay for my weekly shoulder therapy visit?: $1.75.

I fear that the whole system in the USA will have to come crashing down disastrously before anything can be done to improve the situation. There are just too many deeply entrenched well-heeled interests with political connections to permit any sort of meaningful change to take place.

The 59% number on vertical integration is significant, but what's more striking is that voters are identifying the mechanism without having the vocabulary for it. When one company owns the insurer, the PBM, the data analytics platform, and employs the doctors, the "competition" that's supposed to constrain prices doesn't exist. Voters feel that. This data confirms they can name it.

The PBM steering finding is worth highlighting. Prohibiting PBMs from profiting when patients are steered toward higher-priced drugs polls at 37% top priority, but the underlying structure is worse than most voters realize. The three largest PBMs control roughly 80% of the market and are owned by the three largest insurers. The entity deciding which drug you get and the entity profiting from that decision are the same company. That's not a market failure. That's the market working exactly as structured.

Interested to see whether future surveys break out voter awareness of specific integration patterns. The polling shows people know something is wrong. The policy question is whether they can connect "my prescription costs too much" to "my insurer owns my pharmacy benefit manager."